Factor investing… style investing… smart beta… quantitative index portfolios. Different names, but with the same simple idea.

This involves extending simple index-tracking funds, that weigh companies based only on their size (such as the S&P 500 or the Top 40 Index), by considering other attractive company features. These include measurements of value, balance sheet quality, profitability, cash flow management, price, and sales momentum, and many more. The premise remains that these measurements are simple to understand and result in transparent portfolios that adhere to predefined rules and have a low-cost structure. These are the same benefits that millions of investors enjoy through using simple vanilla ETF trackers. But factor funds come with an “active” twist in how the rules are determined.

The factors used to design systematic (rules-based) portfolios represent company features proven to make them more likely to outperform peers over time. These company attributes are generally well known and accepted by active managers and analysts to inform their processes too. Factor portfolios can therefore be regarded as non-vanilla index portfolios, offering the best of both active and passive funds.

Does This Mean More Risk?

Some may view these as more exotic or high-risk strategies, when in truth we apply multi-factor logic in our daily lives. When buying a house, you’d consider multiple factors in contextualising the price. A R5 million house may be a bargain (if situated in Constantia, with four bedrooms and a mountain view) or it may be a ‘lemon’ (if situated next to a highway, with a leaking roof and noisy neighbours – the four-bedroom status may mask its downsides). Simply put, we’d be better off considering more than size or simply using our intuition to determine the case for buying a house (or a portfolio of houses).

Factor strategies allow investors to harvest the long-term factor premiums that research has shown is on offer. Active portfolios with a style bias (e.g., a value manager or a high-quality manager) can deviate from their stated objectives through different market cycles. If cheaper companies underperform for an extended period, it may become intolerable for a value manager not to follow the herd. This may seem perfectly reasonable, until of course value companies rebound strongly and the opportunity for recovery is lost.

Harvesting the Upside

Empirical analysis, globally, has shown that factor indices offer long-term premiums and more consistent upside – provided they are consistently sought. Trying to time factor exposures seldom works. Style diversification is also key to ensuring a smooth return profile with less downside (e.g., considering quality and momentum styles together to best contextualise value). This means factor premiums are not mere short-term arbitrage opportunities, but rather offer long-term upside to those able to harvest it consistently.

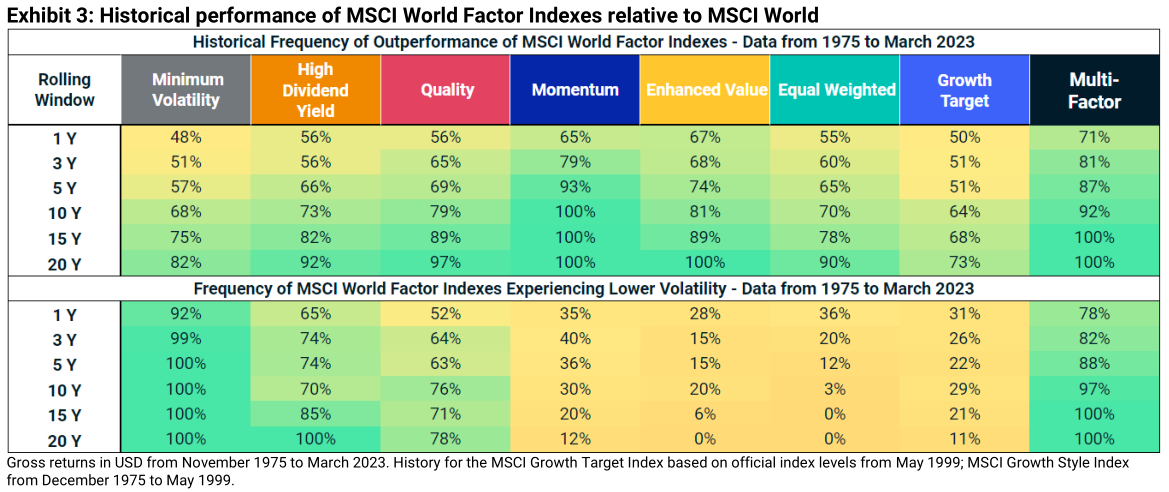

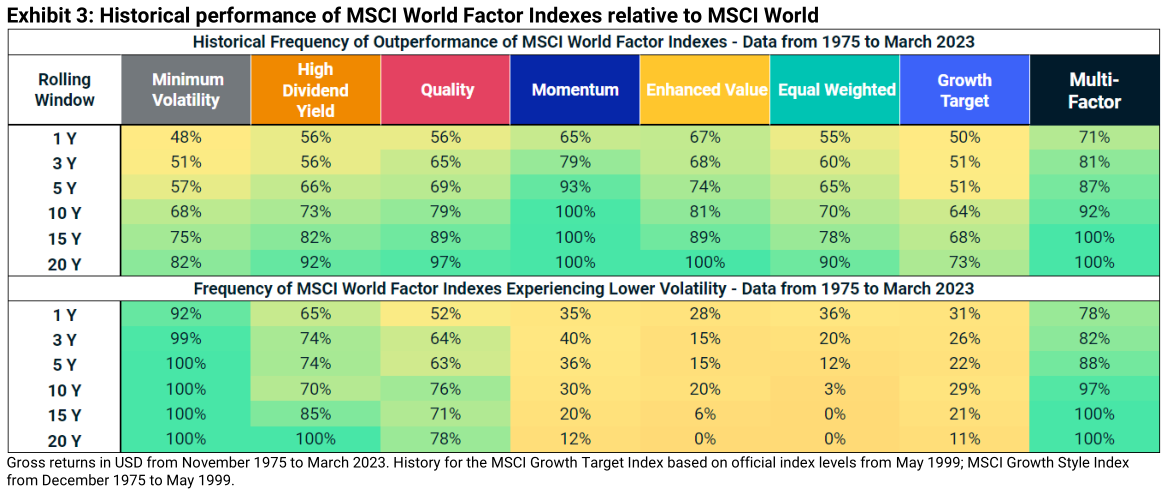

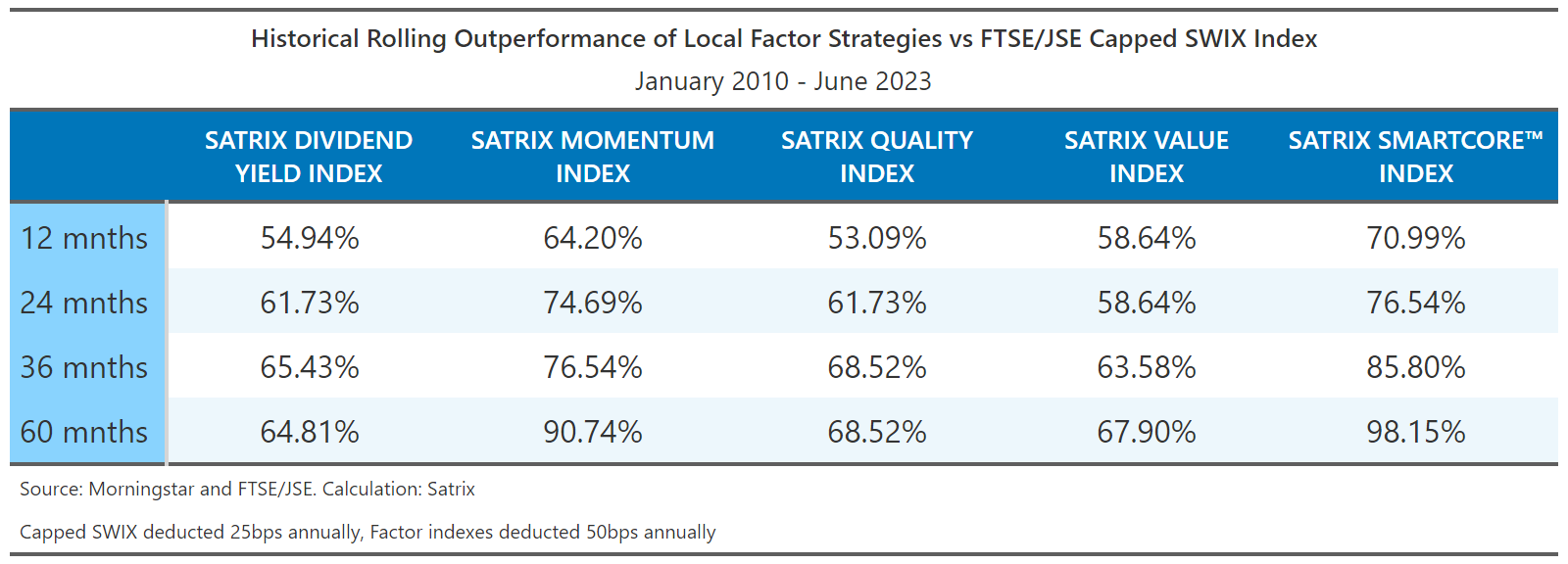

The proof is in the pudding too. Below we show historical performance numbers for global factor indices compared to the MSCI World Index. We also show local Satrix factor indices compared to the Capped SWIX Top 40 Index (methodologically consistent backtests are included prior to inception, where relevant). In both cases, factor strategies show great consistency in outperformance when the holding period is increased (especially for multi-factor indices, such as the MSCI Multi-Factor Indices and Satrix SmartCore™ Index).

In conclusion, factor index strategies offer an efficient, transparent, and low-cost means of refining core equity exposures by considering more than simply the size of a company. These strategies are also not exposed to the lack of style consistency often displayed by style-oriented managers. Factor investing constitutes an attractive blend of being active in the set of rules targeted, but passive in the application of these rules. The result is a best-of-both strategy that is becoming harder to ignore.

Disclosure

*Satrix, a division of Sanlam Investment Management

Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. Satrix Managers is a registered Manager in terms of the Collective Investment Schemes Control Act, 2002.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, their shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Related Content

22 November 2024

Election Impact on Global Markets and Investment Trends Beyond 2024

12 November 2024

Newsletter | October 2024 | Two Years of a Raging Bull Market

In 2022, global markets faced turmoil from the Russia-Ukraine conflict, high inflation, and aggressive rate hikes. By October 2024, markets rebounded.