By Nico Katzke, Head of Portfolio Solutions at Satrix*

The What…

Harmonising the SWIX and ALSI methodologies to have a single representative benchmark index is not a new topic. In fact, over the past few years there’s been much talk about the need for it, with the JSE initiating multiple public discourses on how to make this a reality. In the past, the differences between the SWIX and ALSI methodologies have been significant, making harmonisation a potentially disruptive exercise. Following the natural alignment between the indices in the past few years, the time is now right for harmonisation to occur, given that there are only a few, somewhat arbitrary, remaining differences between the SWIX and ALSI indices. Note for the remainder, we will refer only to the SWIX and not the Capped SWIX as these are virtually equivalent currently following Naspers’ reduced index weight.

The Why…

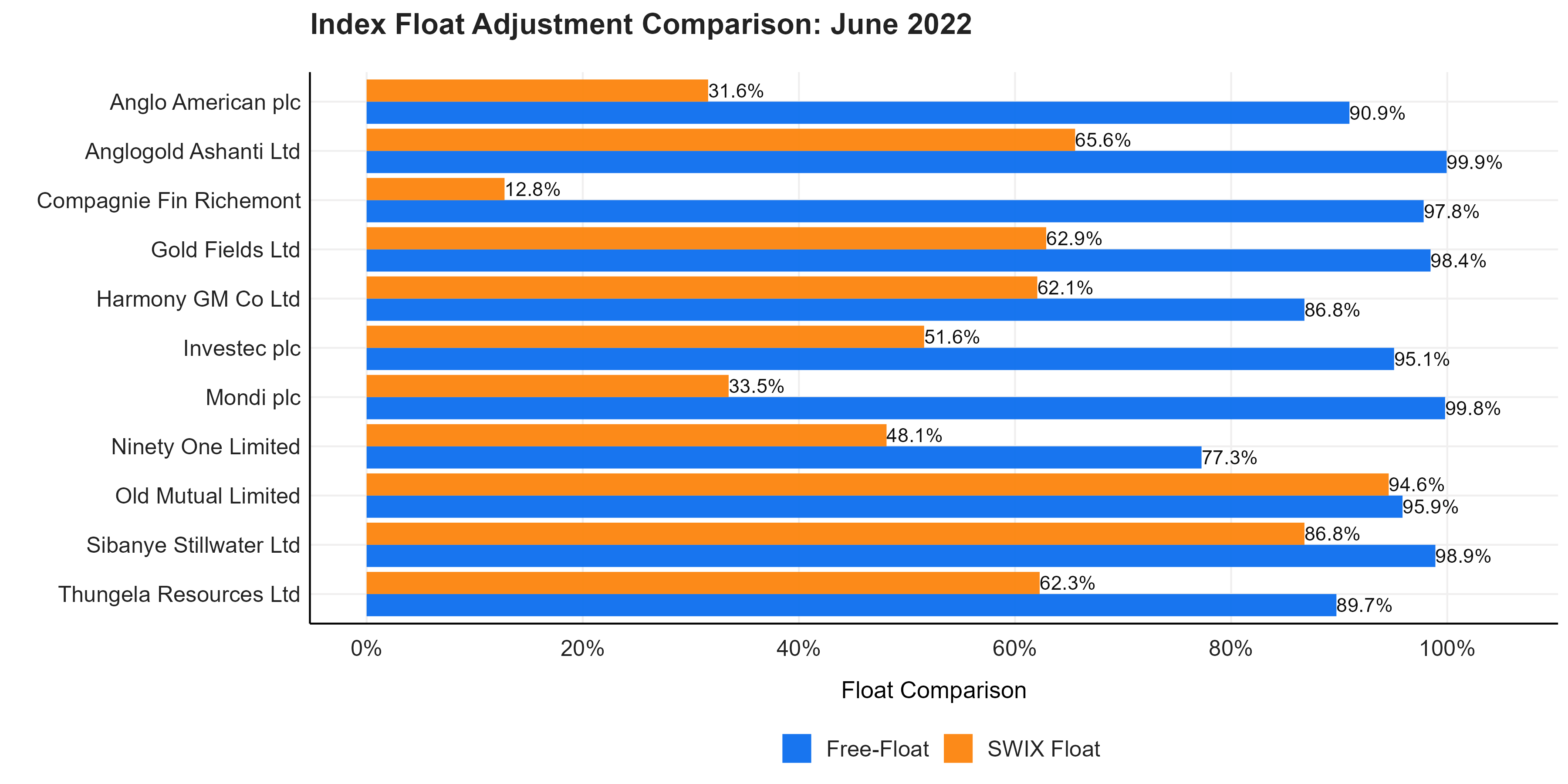

While both the SWIX and ALSI index methodologies consider exactly the same constituents, the free floats for some companies differ. Notably, SA companies that moved their primary listings offshore before October 2011 (called grandfathered companies) are included at their full global float for the ALSI weight calculation1. The SWIX was introduced in 2004 to offer an alternative benchmark that considers only the locally available float on STRATE, thereby down-weighting the grandfathered companies. But corporate actions in recent quarters have meant that most of the float differences, notably for CFR (Richemont), BHG (BHP Group), SAB (South African Breweries), OML (Old Mutual), HAR (Harmony Gold) and GFI (Gold Fields) to name a few, have converged.

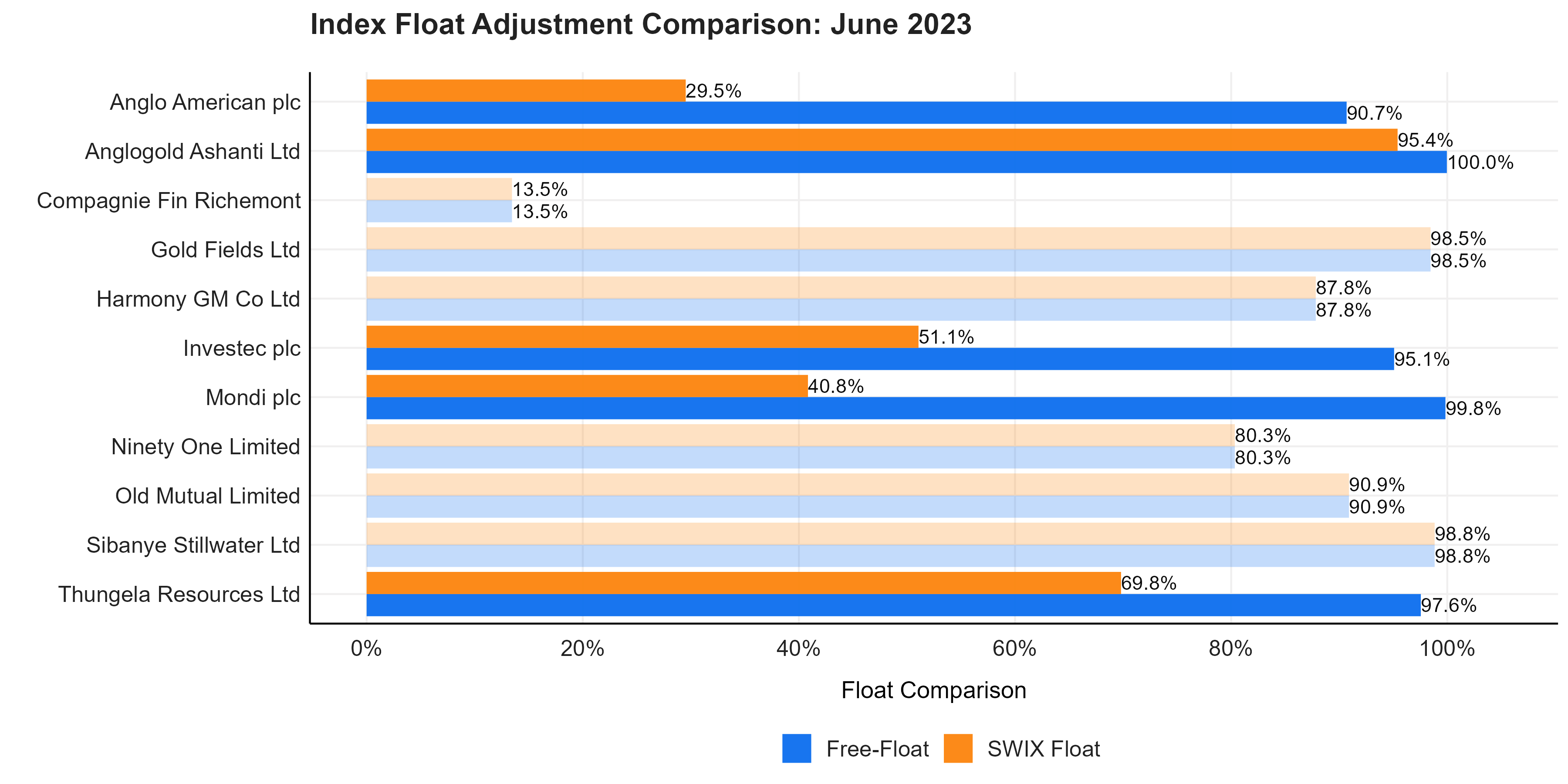

The process of index harmonisation is thus less disruptive today than it would have been in the past. Consider, for example, the companies that had different SWIX and ALSI floats from just a year ago compared to the most recent rebalance in June 2023 (shaded floats on the right means they are currently aligned):

Source: Satrix. Data: FTSE/JSE. 30 June 2022

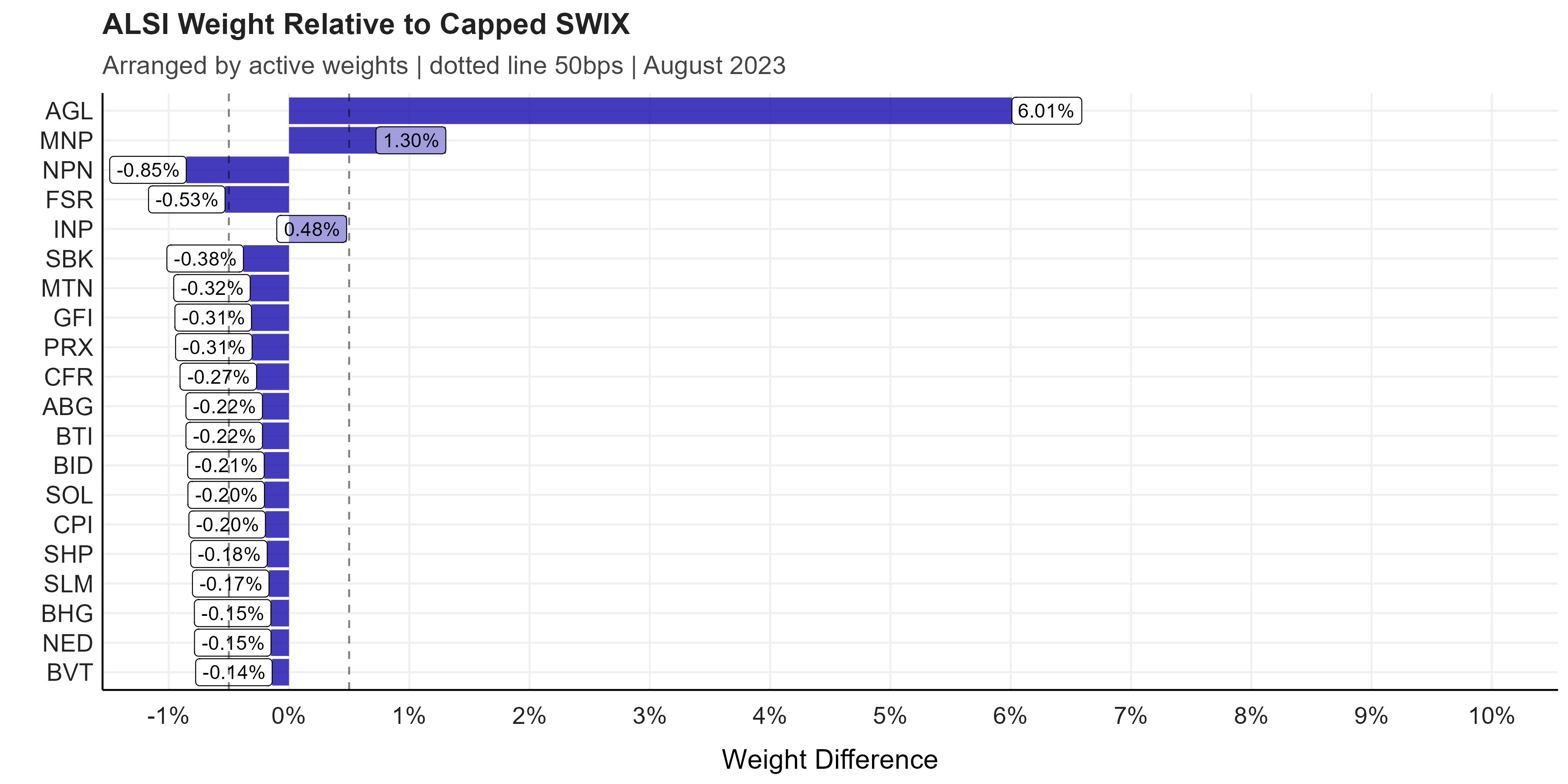

From this, the only meaningful differences currently remaining between the two methodologies are for AGL (Anglo American), INP (Investec Plc) and MNP (Mondi), (with the underweights funding the few remaining grandfathered over-weights):

Source: Satrix. Data: FTSE/JSE. 30 August 2023

The When…

At the March 2024 rebalance, the JSE intends doing away with the ALSI methodology to align the benchmark indices to the SWIX methodology (using companies’ available local float as reflected on STRATE). The new indices will be called All-Share indices, which means all the current SWIX alternatives fall away and the ALSI effectively becomes the SWIX.

Importance

Having a single domestic equity market index is important for several reasons.

First, having multiple benchmark indices creates confusion for investors looking to compare the performance of their managers to an investable alternative. Having a single index will make broad performance comparisons simpler, with more transparency in terms of the value added by active differentiation. Ideally, a benchmark choice should not be a strategic decision.

Second, various managers have begun to benchmark their funds to peer averages. Given that the past two decades have seen the majority of active funds underperform both the ALSI and SWIX index alternatives, a comparison to active manager peers overstates aggregate performance relative to an investable index alternative. By the end of 2022 more than 20% of assets managed actively were done using the industry median as a stated benchmark (Morningstar). Having a single benchmark

index should make peer-relative comparisons harder to motivate, as well as making it easier to know what a relevant and investable market performance would have been.

Conclusion

The performance differences between the SWIX and the ALSI indices have been significant in recent years. We’ve shown in the past that the choice between which index to track is a key strategic decision, with the realised tracking error of the SWIX being as high as the median active manager’s, relative to the ALSI.

Up to the end of June 2023, the one-year return difference between the ALSI and the SWIX was more than 7%, with the difference almost entirely explained by the ALSI’s comparative overweight to one company, Richemont. This meant that active managers with the SWIX as a benchmark would have performed significantly better on a relative basis simply because of one company’s return – an unfortunate function of our index methodology differences.

As the indices have begun to converge following corporate actions in recent years, index harmonisation is now finally achievable with limited disruption. From March 2024, we will finally have a single representative benchmark index for our local equity market. The benefits of this transparency and simplicity cannot be overstated.

*Satrix, a division of Sanlam Investment Management

Satrix Investments (Pty) Ltd is an approved FSP in term of the Financial Advisory and Intermediary Services Act (FAIS). The information does not constitute advice as contemplated in FAIS. Use or rely on this information at your own risk. Consult your Financial Adviser before making an investment decision. Satrix Managers is a registered Manager in terms of the Collective Investment Schemes Control Act, 2002.

While every effort has been made to ensure the reasonableness and accuracy of the information contained in this document (“the information”), the FSPs, its shareholders, subsidiaries, clients, agents, officers and employees do not make any representations or warranties regarding the accuracy or suitability of the information and shall not be held responsible and disclaims all liability for any loss, liability and damage whatsoever suffered as a result of or which may be attributable, directly or indirectly, to any use of or reliance upon the information.

Related Content

25 July 2024

Offshore Equity Markets Soar: A Strong First Half of 2024

The first half of 2024 has been remarkable for offshore equity markets, driven by tech advancements, rate cuts, and pivotal elections.

25 July 2024

Capturing Value for Clients from South Africa’s ETF Boom

ETFs are designed to protect existing investors from the costs generated by others entering or exiting the fund, unlike Unit Trusts. This design feature shields long-term investors from external churn, safeguarding their performance and ensuring a fairer cost structure.